Wine Market Wine is an alcoholic beverage produced by fermentation of grapes and other fruits. There are many health benefits of moderate wine consumption including lowering the risk of heart disease, anti-aging properties, improvement in brain function etc. Wine contains antioxidants called polyphenols that can protect cells from damage. The global wine market consists of red wine, white wine, rose wine and fruit wine. Red wine helps in reducing the risk of stroke while white wine contains heart friendly compounds. The increasing awareness about health benefits of wine is driving more people to include it in their diet. The global wine Market is estimated to be valued at US$ 3422.75 billion in 2024 and is expected to exhibit a CAGR of 30% over the forecast period 2024 to 2031, as highlighted in a new report published by Coherent Market Insights. Market Opportunity: The growing health benefits awareness about moderate wine consumption presents a major market opportunity. More recent studies have further confirmed cardiovascular benefits of red wine along with reduced risk of type 2 diabetes and cognitive decline. As people become increasingly health conscious, they are incorporating wine in their routine owing to its anti-aging properties and reduced disease risk. The wine market players can capitalize on this opportunity by focusing marketing campaigns on highlighting specific health advantages of their products. They can also introduce new product lines specifically targeting the health focused demographic. This will help drive higher demands as well as premiumization in the global wine market during the forecast period. Porter's Analysis Threat of new entrants: The threat of new entrants in the wine market is moderate. While large capital investments and established distribution channels favor incumbent players, new premium and craft wine varietals present opportunities for niche market entry. Bargaining power of buyers: The bargaining power of buyers in the wine market is high. Large retail chains and online platforms negotiate significant discounts and favorable terms from suppliers. Buyers also have many national and international brand options across all price points. Bargaining power of suppliers: The bargaining power of suppliers is moderate. While a few major suppliers dominate raw material provision, especially for popular varietals, availability of contract farming and imports from new regions mitigates supplier leverage. Threat of new substitutes: The threat of substitutes is moderate. While beer and spirits pose competition, wine retains occasions and associations that establish it as a preferred beverage. Product innovation also helps wine varieties adapt to evolving preferences. Competitive rivalry: Competition in the wine market is intense due to the presence of several global and regional players. Players compete on pricing, quality, brand recognition, distribution reach, and targeted promotions. SWOT Analysis Strengths: Wide availability of premium and craft varietals across retail formats such as supermarkets, liquor stores and e-commerce sites boosts sales and consumer exposure. Strong wine cultures in regions like Europe underpin robust domestic demand. Weaknesses: Seasonal harvests and variable vintages expose the industry to supply fluctuations and price volatility. Environmental factors like climate change pose production challenges over the long term. Opportunities: Emerging markets in Asia Pacific and Latin America present significant untapped potential due to rising affluence and experimentation with fine wines. Innovation in organically-farmed, vegan-friendly and lower alcohol styles expand the consumer base. Threats: Trade disputes and tariffs disrupt international supply chains and market access. Strict regulations on branding and marketing limit strategies in some countries. Health consciousness regarding alcohol consumption constrains volume growth. Key Takeaways The Global Wine Market Growth is expected to witness high over the forecast period of 2024 to 2031, fueled by rising disposable incomes in developing nations and the expansion of fine wine culture to new regions. With a projected market size of US$ 3422.75 million in 2024 growing at a CAGR of 30% through 2031, significant opportunities lie ahead for industry players. Europe currently dominates the global wine market, accounting for over 40% revenue share in 2024 due to strong winemaking traditions and per capita consumption levels in countries such as Italy, France and Spain. However, China is anticipated to be the fastest growing regional market, growing at a CAGR of 35% through 2031 as domestic wine consumption increases dramatically among urban households. Key players operating in the wine market are E. & J. Gallo Winery, The Wine Group, Constellation Brands, Castel Group, and Accolade Wines. These players are focusing on geographic expansion, premiumization through sophisticated appellation wines, and product diversification Explore more information on this topic, Please visit- https://www.dailyprbulletin.com/wine-market-share-size-and-growth-share-trends-analysis-demand-forecast-2/

0 Comments

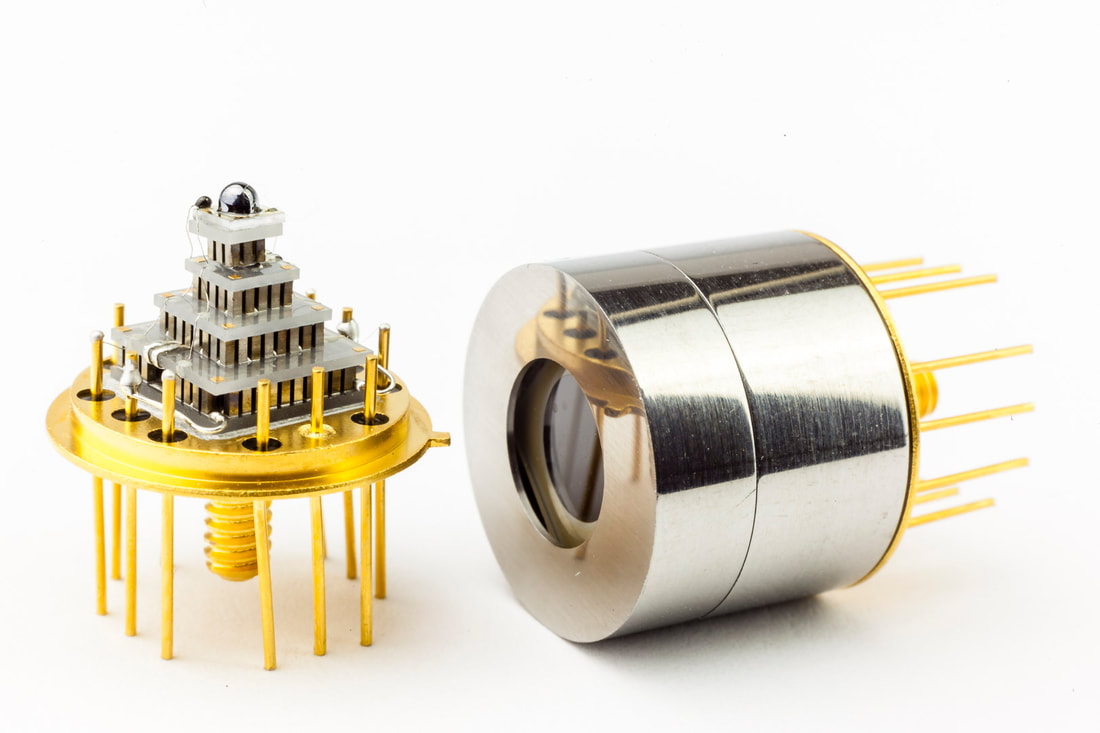

U.S. Nasal Spray Market Nasal sprays are helpful in delivering medication directly into the nasal cavity thereby providing fast relief in conditions like allergic rhinitis, nasal congestion and sinusitis. Nasal sprays offer several advantages over oral medications as they are convenient to use, act quickly and have minimal systemic side effects. Rising instances of allergies due to changing environmental conditions and pollution levels have significantly boosted the demand for nasal sprays in the U.S. The global U.S. Nasal Spray Market is estimated to be valued at US$ 11408.66 Bn in 2024 and is expected to exhibit a CAGR of 7.5% over the forecast period 2024-2031, as highlighted in a new report published by Coherent Market Insights. Market Opportunity: The growing prevalence of allergic rhinitis in the country presents significant opportunities for players in the nasal spray market. According to estimates, allergic rhinitis affects over 50 million Americans annually. Nasal congestion is the most common symptom reported by patients suffering from allergic rhinitis. Since nasal sprays provide quick and effective relief from congestion, manufacturers are developing advanced formulations targeting allergic rhinitis. The increasing R&D focused on designing formulations containing multiple anti-allergy agents is helping expand the reach of nasal sprays among allergic rhinitis patients. This wide therapeutic application and rising investments in innovation are projected to substantially boost the revenues of nasal spray market in coming years. Porter’s Analysis Threat of new entrants: The threat of new entrants is moderate as the U.S. nasal spray market is dominated by major players. However, the entry barrier is low due to low investment and technology requirement. Bargaining power of buyers: The bargaining power of buyers is high due to the presence of many companies providing similar products. Buyers can negotiate for better prices and quality. Bargaining power of suppliers: The bargaining power of suppliers is moderate. Major suppliers include active pharmaceutical ingredients and dispensing equipment manufacturers. Threat of new substitutes: The threat of substitute products like nasal drops and oral medications is moderate. However, nasal sprays have stronger patient compliance. Competitive rivalry: The competitive rivalry is high due to the presence of many global and domestic players offering similar products. Companies compete on pricing, innovation, quality, and brand value. SWOT Analysis Strength: High treatment efficacy in relieving nasal congestion. Rising demand for over-the-counter medicines for quick relief. Weakness: Possible side effects of long-term usage like nasal dryness and irritation. High competition increases marketing expenses. Opportunity: Growing allergy population increases the scope. New product launches addressing unmet needs. Threats: Strict regulatory approvals delay market entry. Patent expiries allow generic competition. Key Takeaways The Global U.S. Nasal Spray Market Growth is expected to witness high. The market size is estimated to reach US$ 20,032.21 million by 2031 from US$ 11,408.66 million in 2024, growing at a CAGR of 7.5% during the forecast period. Regional analysis related content - The Western U.S accounted for the largest share of over 30% in 2020 due to the high pollution levels and prevalence of allergies in states like California and Washington. Key players related content - Key players operating in the U.S. Nasal Spray market are GlaxoSmithKline plc, Sanofi S.A., Bayer AG, Merck & Co., Inc., Novartis AG, Johnson & Johnson Services, Inc., Pfizer Inc., Procter & Gamble, AstraZeneca Plc., NeilMed Pharmaceuticals Inc., Church & Dwight Co., Inc., and Neurelis, Inc. Explore more information on this topic, Please visit- https://www.dailyprbulletin.com/u-s-nasal-spray-market-share-size-and-growth-share-trends-analysis-demand-forecast/  Mid-IR Sensors Market Mid-IR sensors detect infrared light wavelengths between 3 to 15 micrometres. They are used in various industrial applications such as gas analysis, thermal imaging, and quality control due to their ability to detect molecular fingerprints and analyze chemical composition. Mid-IR sensing helps make industrial processes safer through detection of hazardous gases and diagnostic of equipment failures before any dangerous accidents occur. The global Mid-IR Sensors market is estimated to be valued at US$ 36.44 Bn in 2023 and is expected to exhibit a CAGR of 15% over the forecast period 2024 to 2031, as highlighted in a new report published by Coherent Market Insights. Market Opportunity: Industrial safety and process monitoring applications present a major market opportunity for mid-IR sensors. Mid-IR sensors are increasingly being used to detect hazardous gases in industrial areas and monitor industrial processes in real-time to avoid accidents and downtime. They allow detection of small gas leaks and help prevent explosions. Mid-IR cameras integrated with sensors are also being used for thermal imaging to detect hot spots in electrical equipment and diagnose equipment issues. This improves safety and uptime of industrial operations. The ability of mid-IR sensors to non-invasively analyze chemical composition further helps optimize industrial processes and quality control. The growth in process automation and focus on workplace safety will drive the demand for mid-IR sensors from various industries like oil & gas, chemicals, and manufacturing over the forecast period. Porter's Analysis Threat of new entrants: Low-mid setup costs makes threat of new entrants moderate as its easy to enter the market however intellectual property rights restrict entry. Bargaining power of buyers: Moderate as buyers have a variety of suppliers to choose from but price is key decision factor. Bargaining power of suppliers: Low as raw materials like MEMS, lenses are supplied by many players globally making suppliers replaceable. Threat of new substitutes: Low as mid-IR technology is specialized with no close substitutes. Competitive rivalry: High as major players compete on technology, price and product differentiation. SWOT Analysis Strength: Robust product pipeline, strong R&D capabilities. Established distribution channels. Weakness: High R&D costs, technology obsolescence risk. Dependence on few industries like military, industrial. Opportunity: Growth in industrial and healthcare sectors. Scope in emerging applications like environmental monitoring. Threats: Commoditization risk. Stringent regulations. Intense competition. Key Takeaways The Global Mid-IR Sensors Market Growth is expected to witness high between 2024 to 2031. The market size in 2024 was US$ 36.44 Bn and is forecast to grow at a CAGR of 15% during the forecast period. Regional analysis: Asia Pacific region is expected to grow the fastest during the forecast period supported by strong economic growth in major country like China, India which is driving adoption of mid-IR technology in application like quality control, pollution monitoring. Key players: Key players operating in the Mid-IR Sensors market are Nestlé S.A, Nissin Food Holdings Co., Ltd., Indofood CBP Sukses Makmur Tbk PT, Tingyi (Cayman Islands) Holding Corporation, Uni-President Enterprises Corporation, Acecook Vietnam Joint Stock Company. Major players are focused on new product development and expansion in emerging markets to strengthen market presence. Explore more information on this topic, Please visit- https://www.dailyprbulletin.com/mid-ir-sensors-market-share-size-and-growth-share-trends-analysis-demand-forecast/  Hard Seltzer Market Hard seltzer is a fermented alcoholic beverage made with water, yeast, sugar, and natural flavorings. Hard seltzers provide the refreshing taste of seltzer along with the buzz of alcohol and have low to zero carbohydrates and calories. The category has gained immense popularity among health-conscious millennial consumers in recent years. Hard seltzers serve as an enjoyable alternative to beer and cocktails for occasions like summer barbecues, outdoor activities, and casual get-togethers. The taste profiles available in hard seltzers satisfy varied preferences and have made the category appealing to both seltzer and beer drinkers. The global Hard Seltzer Market is estimated to be valued at US$ 7.65 Bn in 2024 and is expected to exhibit a CAGR of 14.9%over the forecast period 2024-2031, as highlighted in a new report published by Coherent Market Insights. Market Opportunity: New product innovation in terms of innovative flavors and varieties presents a major market opportunity for hard seltzer producers. Existing hard seltzer producers are investing in R&D to develop new flavors beyond the common lemon-lime, black cherry, and mango varieties currently dominating the market. Exotic fruit flavors, seasonal flavors tied to holidays or regional fruits, and even savory flavors offer opportunities to attract new consumers and boost existing consumer loyalty. Innovation in varieties including spiked seltzers with different alcohol percentages, cocktail-inspired flavors, and specialty limited edition varieties keeps consumer interest high. With experimentation, hard seltzers have potential to disrupt other beverage categories as well. Significant investments and focus on constant innovation will enable hard seltzer brands to cement their hold in the lucrative market. Porter’s Analysis Threat of new entrants: The hard seltzer market has moderate threat of new entrants as it requires large capital investments and economies of scale due to varied packaging and flavor requirements. However, the booming market offers opportunities for premiumization and new flavors. Bargaining power of buyers: Buyers in the form of distributors and retailers have moderate bargaining power due to the presence of several established brands and new product launches regularly. However, private labels offer alternatives. Bargaining power of suppliers: Suppliers of raw materials like aluminium and malt have moderate bargaining power due to the availability of substitute raw materials. Threat of new substitutes: The threat from substitutes like beer, wine and spirits is moderate to high since hard seltzer appeals to the same target audience. Product differentiation is a key strategy. Competitive rivalry: The market is highly competitive with focus on flavor innovation, brand marketing and expansion to grocery retail channels. SWOT Analysis Strengths: Growing health consciousness. Flavor innovations. High social media engagement of brand promotions. Weaknesses: Vulnerable to taxes and regulations on alcohol content. Seasonality affects summer-focused sales. Opportunities: Expanding demographics and occasions of consumption. Product line extensions into spirits seltzers. Threats: Substitutes from beer and wine companies. Intense competition diminishing margins. Key Takeaways The Global Hard Seltzer Market Growth is expected to witness high over the forecast period of 2024 to 2031 supported by new product launches, innovative flavors and expanding retail availability beyond bars and restaurants. The global Hard Seltzer Market is estimated to be valued at US$ 7.65 Bn in 2024 and is expected to exhibit a CAGR of 14.9%over the forecast period 2024-2031. Regional analysis indicates North America currently dominates the market led by the US. However, Europe is witnessing rising demand driven by the UK, Spain and Germany. Key players operating in the hard seltzer market are Hindalco Industries Ltd.; Arconic Corp.; Norsk Hydro ASA; Constellium N.V.; Kaiser Aluminum; Alupco; Gulf Extrusions Co. LLC; Balexo Bahrain Aluminium Extrusion Company; QALEX. Leading alcoholic beverage companies are launching their own hard seltzer brands such as White Claw by Mark Anthony Brands and Truly Hard Seltzer by Boston Beer Company. Private label products also offer competition. Innovation will be the key differentiating factor in this highly competitive landscape going forward. Explore more information on this topic, Please visit- https://www.dailyprbulletin.com/hard-seltzer-market-share-size-and-growth-share-trends-analysis-demand-forecast/  GLP-1 Receptor Agonist Market GLP-1 receptor agonists are incretin-based therapies used for the management of type 2 diabetes. GLP-1 receptor agonists work by stimulating the release of insulin from beta cells of pancreas and suppressing glucagon release from alpha cells in a glucose-dependent manner. This helps in maintaining normal blood glucose levels with minimal hypoglycemia risk. The rising prevalence of diabetes worldwide has increased the need for effective antidiabetic drug therapies with fewer side effects. The global GLP-1 receptor agonist market is estimated to be valued at US$ 11.5 billion in 2023 and is expected to exhibit a CAGR of 17.8% over the forecast period 2024 to 2031, as highlighted in a new report published by Coherent Market Insights. Market Opportunity: The growing diabetes population worldwide represents a major market opportunity for GLP-1 receptor agonists. As per the International Diabetes Federation, approximately 537 million adults (20-79 years) were living with diabetes in 2021, with the number projected to rise to 643 million by 2030 and 783 million by 2045. The prevalence is increasing due to lifestyle changes, obesity and lack of physical activity. With the majority of diabetes cases being type 2 diabetes, GLP-1 receptor agonist drugs that effectively control blood glucose levels with lower risk of adverse effects are expected to gain widespread adoption among patients and physicians. This opens up major opportunity for manufacturers to capitalize on the benefits offered by GLP-1 receptor agonists and strengthen their presence in the diabetes care market. Porter’s Analysis Threat of new entrants: The threat of new entrants is moderate as the biopharma industry requires significant capital investment and licensing to enter the market. However, opportunities exist for specialty generics and biosimilars. Bargaining power of buyers: The bargaining power of buyers is moderate to high as major pharmaceutical companies and insurance providers can negotiate lower drug prices. Bargaining power of suppliers: Suppliers of active pharmaceutical ingredients and contract manufacturing organizations have some bargaining power. Threat of new substitutes: New drug delivery technologies and therapeutic areas pose a threat of substitution over time. Competitive rivalry: Intense as major players compete through innovative drug formulations, pricing strategies, and marketing. SWOT Analysis Strengths: Established efficacy and safety profiles of leading drugs; significant clinical trial data; growing patient pool. Weaknesses: High development costs; strict regulatory pathways; patent cliffs on leading brands. Opportunities: Expanding into new indications; combinations with other therapies; emerging markets growth. Threats: Biosimilar competition; reimbursement pressures; side effect safety concerns. Key Takeaways The Global GLP-1 Receptor Agonist Market Demand is expected to witness high growth during the forecast period of 2024 to 2031. The growth is attributed to rising prevalence of type 2 diabetes and obesity globally. Regional analysis shows that North America currently dominates the market due to presence of major players and higher disease prevalence compared to other regions. The Asia Pacific region is expected to grow at the fastest pace during the forecast period. Key players operating in the GLP-1 Receptor Agonist market are Novo Nordisk, Eli Lilly, AstraZeneca, Sanofi, Boehringer Ingelheim, and others. Novo Nordisk leads with its branded drugs Victoza, Saxenda and Ozempic while Eli Lilly is a strong player with Trulicity. Players are focused on expanding to new geographical territories and drug formulations. Explore more information on this topic, Please visit- https://www.dailyprbulletin.com/glp-1-receptor-agonist-market-share-size-and-growth-share-trends-analysis-demand-forecast-2/  Global Radar Speed Gun Market Radar speed guns are designed for use by law enforcement officials to measure vehicle speed and detect infractions for enforcement of speed limits without apprehending violators. They offer non-contact speed detection using a radar beam aimed at an oncoming or passing vehicle. The global radar speed gun market demand has increased significantly for traffic enforcement to reduce road accidents and enhance safety. The global Radar Speed Gun Market is estimated to be valued at US$ 1637.57 Bn in 2024 and is expected to exhibit a CAGR of 25% over the forecast period 2024 to 2031, as highlighted in a new report published by Coherent Market Insights. Market Opportunity: The increased adoption of radar speed guns for traffic enforcement presents a major market opportunity. Law enforcement agencies across the globe are increasingly deploying radar speed guns to regulate traffic effectively and reduce accidents. According to the World Health Organization, speeding is a key risk factor for road traffic crashes worldwide. Adopting radar speed guns allows strict monitoring of speed limits without having to physically stop vehicles. This facilitates better enforcement of speed limits across multiple lanes simultaneously without disruptions. The growing focus on road safety will continue driving the adoption of radar speed guns globally during the forecast period. Porter's Five Force Analysis The threat of new entrants: The costs associated with R&D, manufacturing, marketing, and distribution create significant barriers to entry for new competitors. Established brands have strong brand loyalty that new entrants must try to overcome. Bargaining power of buyers: Buyers have moderate bargaining power. There are multiple established suppliers of radar speed guns providing substitutable products. However, switching costs are relatively low. Bargaining power of suppliers: Component suppliers have low bargaining power due to the availability of substitute components and parts. Suppliers are also easily replaced. Threat of new substitutes: There is moderate threat of substitution from other speed detection technologies such as lidar. However, radar speed guns offer cost advantages over substitutes. Competitive rivalry: The global radar speed gun market is fragmented with the presence of several international and regional players. Competition is based on product features and pricing. SWOT Analysis Strengths: Radar speed guns provide non-contact, accurate speed measurement. They are easy to operate and maintain. Weaknesses: High initial costs. Require periodic calibration and servicing. Susceptible to environmental factors like weather. Opportunities: Growth in usage by law enforcement and traffic departments. Rising safety concerns are increasing adoption. Threats: Substitution threat from alternative speed detection technologies. Economic slowdowns can decrease procurement. Key Takeaways The Global Radar Speed Gun Market Size is projected to reach US$ 1637.57 Bn by 2024 growing at a CAGR of 25% during the forecast period. Regional analysis: North America dominates the market currently owing to strict road safety laws. Asia Pacific is expected to witness the highest growth driven by increasing investment in road infrastructure and safety adoption in major countries like China and India. Key players: Key players operating in the global radar speed gun market are AT&T Inc., Fujitsu Ltd., Kyndryl (IBM Corporation), Wipro Ltd, Orange SA, Telefónica SA, Samsung Electronics Co. Ltd, Hewlett-Packard, Vodafone Group PLC, Microsoft Corporation, Tech Mahindra. These companies are focusing on developing advanced and customized solutions to strengthen their market position. Explore more information on this topic, Please visit- https://www.dailyprbulletin.com/global-radar-speed-gun-market-share-size-and-growth-share-trends-analysis-demand-forecast  Global Cloud Migration Service Market Cloud migration services help organizations move workloads, applications, and data to the cloud. This facilitates enterprises to leverage features such as agile infrastructure, on-demand resources, higher scalability, and disaster recovery. Cloud migration ensures business continuity and optimized performance of applications by moving them from on-premises IT infrastructure to cloud environments such as public, private or hybrid cloud. The global Cloud Migration Service Market is estimated to be valued at US$ 7.88 Mn in 2024 and is expected to exhibit a CAGR of 4.6% over the forecast period 2024-2031, as highlighted in a new report published by Coherent Market Insights. Market Opportunity: Migrating to cloud provides enterprises with improved efficiency and scalability. Applications hosted on cloud can easily scale up or down depending on real-time computing needs. This helps companies optimize infrastructure costs as they pay only for the resources utilized. Further, cloud platforms offer self-service provisioning allowing IT teams to instantly deploy resources on demand. Automated cloud processes also enhance operational efficiency by reducing manual efforts. Migrating to cloud empowers enterprises with an agile environment to efficiently support business growth. Porter's Analysis Threat of new entrants: The global cloud migration service market witnesses moderate threat of new entrants due to high capital requirement and presence of key global market players. Bargaining power of buyers: The bargaining power of buyers is moderate due to availability of alternatives and price sensitivity for cloud migration services. Bargaining power of suppliers: The bargaining power of suppliers is moderate due to availability of substitutes and integration of suppliers. Threat of new substitutes: Threat of new substitutes is low as there are limited options for cloud migration services. Competitive rivalry: The competitive rivalry is high due to presence of key global players. SWOT Analysis Strength: Cloud migration services aim to enhance IT infrastructure, optimize operational costs, and improve scalability for businesses. Migration ensures high availability, scalability, data security and reduces service downtime. Weakness: Complexity of migrating legacy applications and lack of in-house IT expertise poses challenges. Concerns over data security and privacy during migration also impacts adoption. Opportunity: Growing inclination of SMEs towards cloud and benefits of digital transformation provide major market opportunities. Rising demand for analytics-as-a-service and disaster recovery-as-a-service supplements growth. Threats: Higher initial investment and recurring costs hamper the market particularly for smaller enterprises. Interoperability issues and vendor lock-in pose threats. Key Takeaways The Global Cloud Migration Service Market Growth is expected to witness high over the forecast period. The global Cloud Migration Service Market is estimated to be valued at US$ 7.88 Mn in 2024 and is expected to exhibit a CAGR of 4.6% over the forecast period 2024-2031. North America dominates the global market owing to high adoption of advanced cloud solutions among enterprises to optimize business processes. Growing demand for cloud-based solutions among healthcare, BFSI, and IT and telecom industries supplements regional growth. Key players operating in the global cloud migration service market are Archer Daniels Midland Company, Jungbunzlauer Suisse AG, Basel, Pfizer Inc., Shandong Juxian Hongde Citric Acid Co. Ltd., Delek Group, Cargill, Incorporated, Weifang Ensign Industry Co. Ltd., Tate & Lyle plc., COFCO Biochemical (AnHui) Co. Ltd., and RZBC GROUP. These players are focusing on new product launches and partnerships to gain competitive advantage in the market. Explore more information on this topic, Please visit- https://www.dailyprbulletin.com/global-cloud-migration-service-market-share-size-and-growth-share-trends-analysis-demand-forecast/ Explore more trending article related this topic: https://www.ukwebwire.com/china-continuous-glucose-monitoring-devices-market-trends-size-and-share-analysis/  Functional Ingredients Market Functional ingredients are compounds or substances that provide health benefits beyond basic nutrition. These ingredients include vitamins, minerals, fibers & specialty proteins, probiotics, minerals, amino acids and others. Functional ingredients are used across various industries like food & beverage, personal care, pharmaceuticals and others. They provide numerous health benefits like improved heart health, vision health, bone health, digestive health, immunity and weight management. The global Functional Ingredients Market is estimated to be valued at US$ 94.31 Mn in 2023 and is expected to exhibit a CAGR of 5.3% over the forecast period 2024 to 2031, as highlighted in a new report published by Coherent Market Insights. Market Opportunity: The wide range of applications of functional ingredients across different industries is estimated to drive the growth of the market. Functional ingredients find applications in various industries like food & beverage, personal care, nutraceuticals and others. For instance, in food & beverage industry, functional ingredients are used in dairy products, bakery products, sports & energy drinks, infant formulas and other products. In personal care industry, they are used in anti-aging creams, acne treatments, sun protection products and others. Growing demand for customized functional food and beverages due to increasing health awareness will further create growth opportunities for functional ingredients market over the forecast period. Porter's Analysis Threat of new entrants: New entrants face high entry barriers in the form of high R&D and manufacturing costs required to produce functional ingredients. Bargaining power of buyers: Buyers have moderate bargaining power as there are many established manufacturers providing substitutable functional ingredients. Bargaining power of suppliers: Suppliers of raw materials have low to moderate bargaining power due to availability of substitute raw material sources. Threat of new substitutes: Threat from substitute is moderate as manufacturers are bringing constant innovation in functional ingredients. Competitive rivalry: Intense competition exists between established players. SWOT Analysis Strength: Wide applications in food and beverages industry. Growing health consciousness boosting demand. Weakness: High costs associated with R&D and compliance with stringent regulations. Fluctuating prices of raw materials. Opportunity: Emerging markets offer high growth potential. Increasing demand for dietary supplements and nutraceuticals. Threats: Supply chain disruptions and trade barriers can impact availability. Stringent regulatory norms across regions. Key Takeaways The Global Functional Ingredients Market Size is expected to witness high growth over the forecast period. The global Functional Ingredients Market is estimated to be valued at US$ 94.31 Mn in 2023 and is expected to exhibit a CAGR of 5.3% over the forecast period 2024 to 2031. The market in North America region currently dominates due to robust functional food and beverage industry and health conscious population. However, Asia Pacific region is expected to grow at fastest pace owing to rising consumer spending on health supplements in countries like China and India. Key players operating in the functional ingredients market are Alkremes Plc., Teva Pharmaceutical Industries Ltd., Glenmark Pharmaceuticals, Titan Pharmaceuticals, Inc., Pfizer, Inc., GlaxoSmithKline plc., Johnson & Johnson, Perrigo Company plc., Cipla Limited, Hikma Pharmaceuticals Plc., Dr. Reddy€TMs Laboratories Limited, Indivior Inc., and Mylan N.V. These companies are focusing on new product launches and capacity expansions to strengthen their market position. Explore more information on this topic, Please visit- https://www.dailyprbulletin.com/functional-ingredients-market-share-size-and-growth-share-trends-analysis-demand-forecast/ Explore more trending article related this topic: https://www.ukwebwire.com/healthcare-staffing-market-propelled-by-increasing-demand-for-dedicated-health-workers/  Data Center Construction Market Data center construction involves building a facility that houses computer systems and associated components like telecommunications and storage systems. It typically includes electrical and mechanical rooms, telecommunications and cable management systems, and various security devices. There has been a rise in demand for cloud-based solutions and services in recent years due to cloud computing capabilities like ubiquitous network access, on-demand self-service, location-independent resource pooling and rapid elasticity. With increased adoption of cloud, enterprises are migrating their infrastructure and services to cloud-based models which require construction of modern hyper-scale data centers. The global Data Center Construction Market is estimated to be valued at US$ 72099.62 Mn in 2023 and is expected to exhibit a CAGR of 6.4% over the forecast period 2024 to 2031, as highlighted in a new report published by Coherent Market Insights. Market Opportunity: The rising demand for cloud-based solutions and services creates a huge opportunity for data center construction market. Cloud computing has emerged as a strategic business model over the last decade and its adoption has increased exponentially across all industry verticals and business segments. Enterprises are deploying cloud platforms for various mission critical workloads which store and process huge amounts of data on a daily basis. This growing dependency on cloud infrastructure is prompting cloud service providers to invest heavily in construction of new modern hyper-scale data centers or expansion of their existing data center facilities. Over the forecast period, this rapid deployment of cloud-based IT infrastructure around the world will drive the demand for data center design and construction on a global scale. Porter’s Analysis Threat of new entrants: The data center construction market requires significant capital investments and economies of scale which pose barriers for new companies. Projects also require specialized skills and certifications. Bargaining power of buyers: Large cloud service providers and hyperscale companies have significant bargaining power over construction companies and vendors due to their scale and demand. Bargaining power of suppliers: Key material suppliers for data centers like power infrastructure providers have some bargaining power given specialized nature of their products and services. Threat of new substitutes: There are no cost effective substitutes for data centers currently. Edge computing is a potential threat in future. Competitive rivalry: The global market is fragmented with presence of global and regional construction players. Intense competition on pricing and timelines. SWOT Analysis Strength: Growing demand for cloud services and data analytics is driving the need for new data centers globally. Hyperscale operators pursue large turnkey projects. Weakness: Construction delays due to supply chain issues, design defects, cost overruns and delays in obtaining regulatory clearances for large projects. Opportunity: Rising demand in developing regions of Asia Pacific and Latin America. Growth in hybrid infrastructure models. Threats: Environmental concerns around large energy consumption of data centers. Dependency on limited component suppliers increases disruption risks. Key Takeaways The Global Data Center Construction Market Growth is expected to witness high over the forecast period driven by increasing digital transformation across industries. The global data center construction market is estimated to be valued at US$ 72099.62 Mn in 2024 and is expected to exhibit a CAGR of 6.4% over the forecast period 2024 to 2031. North America currently dominates the market due to high density of hyperscale operators and strong government support for development of local data center infrastructure. The Asia Pacific region is anticipated to be the fastest growing market with China, India, Japan, Australia and New Zealand emerging as major data center hubs. Key players operating in the data center construction market are Regeneron Pharmaceuticals, Inc., Alimera Sciences, Oxurion NV., Abbvie Inc. and F. Hoffmann-La Roche Ltd. These companies are investing in large-scale build outs to meet growing cloud demand. Despite supply chain challenges, major operators pursued modular data center development during the pandemic to augment capacity. Growth opportunities lie in greenfield projects for hyperscale campuses and retail colocation facilities to address the rising edge computing needs. Explore more information on this topic, Please visit- https://www.dailyprbulletin.com/data-center-construction-market-share-size-and-growth-share-trends-analysis-demand-forecast/ Explore more trending article related this topic: https://www.pressreleasebulletin.com/digital-trust-market-size-and-trends-analysis/  Rubber Dumbbells Market Rubber dumbbells are versatile weights that provide a cost-effective method for strength training at home or in commercial gyms. They allow for muscle development through weight lifting and also provide cardio enhancements when incorporated into high-intensity interval training. With a soft, foam interior and durable rubber exterior, they provide a safe and comfortable gripping surface during exercise. The global rubber dumbbells market is estimated to be valued at US$ 229.94 million in 2023 and is expected to exhibit a CAGR of 5.9% over the forecast period 2024 to 2031, as highlighted in a new report published by Coherent Market Insights. Market Opportunity: The growing health and fitness trends among consumers present a major market opportunity for increased sales of rubber dumbbells and other home exercise equipment. Personal health and fitness have risen up consumer priority lists in recent years, driven by factors like increasing obesity rates and a greater focus on preventative healthcare. As more people incorporate regular exercise into their daily routines, the demand for affordable home gym options continues to grow substantially. Rubber dumbbells provide an accessible and versatile solution for muscle-building workouts at home. Manufacturers that offer innovative rubber dumbbell designs, along with comprehensive online workout programs and tutorials, are well-positioned to gain increased market share as consumers continue prioritizing their health. Porter's Analysis Threat of new entrants: The rubber dumbbells market has moderate threat of new entrants due to established customers and high initial costs required for setting up production facilities. However, growing popularity of home fitness is providing opportunities. Bargaining power of buyers: The bargaining power of buyers is high in this market as rubber dumbbells have numerous substitutes. Buyers can easily switch to other inexpensive alternatives. Bargaining power of suppliers: A few key manufacturers supply rubber dumbbells. This gives them significant bargaining power over buyers. Suppliers also differentiate their products to maintain strong position. Threat of new substitutes: Substitutes like steel and plastic dumbbells as well as resistance bands pose high threat. Their lower costs is a major factor. Competitive rivalry: The market has presence of numerous regional and global players competing on pricing and product innovations. SWOT Analysis Strength: Rubber provides durability. Growing health and fitness trends boost demand. Weakness: High manufacturing costs. Easy availability of substitutes. Opportunity: Emerging online retail channels. Rising incomes in developing nations. Threats: Threat from other flexible and inexpensive substitutes. Intense competition. Key Takeaways The Global Rubber Dumbbells Market Growth is expected to witness high. The global Rubber Dumbbells Market is estimated to be valued at US$ 229.94 Mn in 2024 and is expected to exhibit a CAGR of 5.9% over the forecast period 2024 to 2031. North America dominates currently due to strong economic conditions and health awareness. Asia Pacific is poised to grow at fastest pace due to increasing health consciousness, growing disposable incomes and expansion of retail infrastructure in major countries like China and India. Key players operating in the rubber dumbbells market are Novartis AG (Switzerland), Biogen Inc. (US), Gilead Sciences, Inc. (US), Bristol-Myers Squibb (US), Alnylam Pharmaceuticals, Inc. (US), and Sarepta Therapeutics, Inc. (US) among others. Key players differentiate through product designs and innovations to augment sales. Explore more information on this topic, Please visit- https://www.dailyprbulletin.com/rubber-dumbbells-market-share-size-and-growth-share-trends-analysis-demand-forecast/ |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

March 2024

Categories |

RSS Feed

RSS Feed